Avalanche RWA: 2025 Recap

Avalanche’s 2025 RWA growth reflects a shift to deployable finance. Stablecoin integration and scaling assets demonstrate how institutional adoption utilizes established blockchain rails.

Everyone is talking about tokenization right now. The better question is why it suddenly feels real? Because the conversation has shifted from interesting to deployable. When governance, compliant issuance, and distribution rails are treated as the starting point, tokenization stops being a concept and starts looking like infrastructure.

If you only followed price charts in 2025, you might have missed the more important story: RWAs kept getting more operational. Less debate about what tokenized assets could become, more work shipping the unglamorous pieces like custody integrations, settlement workflows, and real distribution.

That’s where Avalanche keeps showing up in a practical way. Fast finality, predictable execution, and the ability to launch purpose-built networks give teams a path to build RWA systems that behave like real financial rails, with controls and throughput designed for production.

RWAs On Avalanche: The 3-Year Step Change

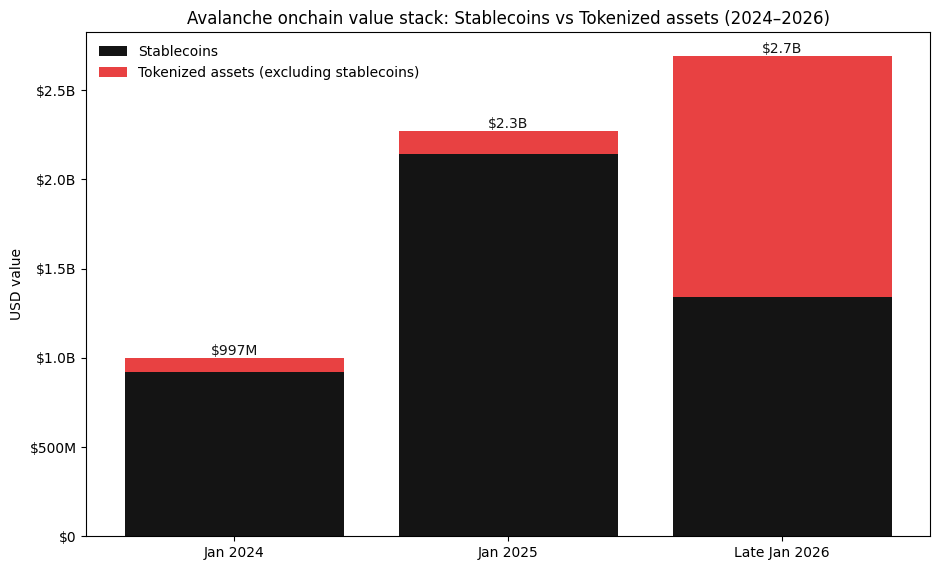

Avalanche’s RWA growth over the last three years is easiest to understand as three clear phases: a real but small base in 2024, early credibility and expansion in 2025, and a scale jump in 2026 that signals institutional deployment.

2024: The baseline

In January 2024, Avalanche had around $74.4M in tokenized assets excluding stablecoins. If we include stablecoins as the settlement layer, the total stack was about $985M (with ~$922.9M in stablecoins). That’s not “nothing,” but it’s still the stage where RWAs are proving they can exist onchain with workable issuance and custody flows, while stablecoins carry most of the day-to-day value movement.

2025: The credibility year

By January 2025, tokenized assets excluding stablecoins reached about $130.1M, roughly a 1.75x increase year over year. At the same time, the total stack (RWAs + stablecoins) rose to about $2.27B, led by ~$2.14B in stablecoins. The important signal is the mix: stablecoins still dominate as the liquidity base, but the non-stablecoin RWA layer is expanding and starting to reflect more institution-friendly structures, which is what “serious issuers are comfortable launching” looks like in practice.

2026: The scale year

By late January 2026, tokenized assets excluding stablecoins hit about $1.35B. That’s roughly 10x growth from January 2025 and about 18x compared to early 2024. Total value including stablecoins was about $2.82B, with stablecoins at roughly $1.34B. This is the inflection point: RWAs stop being a thin layer on top of stablecoin liquidity and become a core part of the onchain asset stack.

What the trend really means

Across 2024 to 2026, the impact is not just “more value on a chart.” It’s that Avalanche moved from testing tokenization to hosting it at scale (RWAs excluding stablecoins becoming a major share of total value), which is what it looks like when tokenization starts behaving like real financial infrastructure.

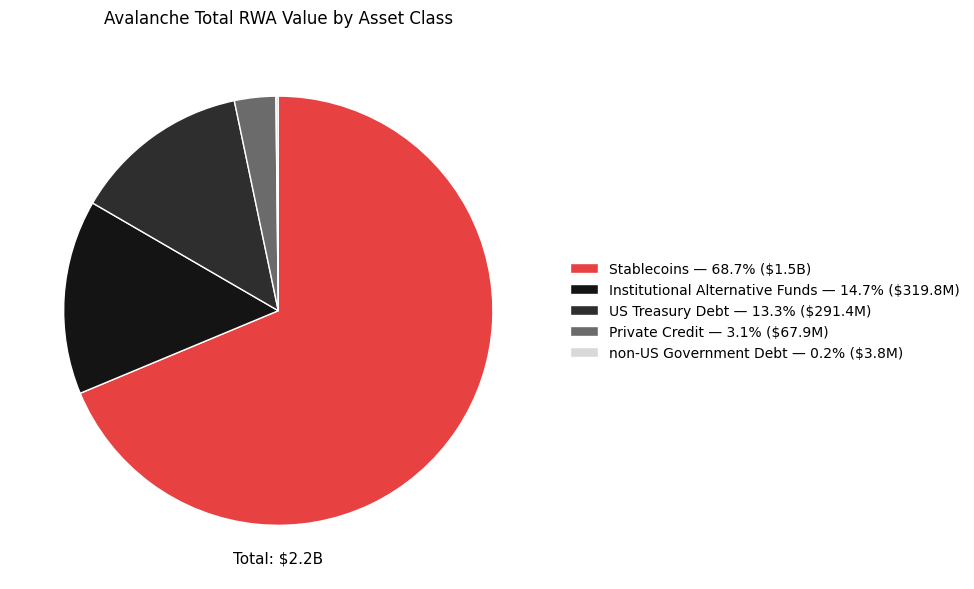

Avalanche RWA Assets By Asset Class

Avalanche’s total RWA value is best understood as a stack with two layers: stablecoins as the liquidity base, and tokenized yield and credit as the growth layer. In the snapshot here, the full pie totals roughly $2.18B, led by stablecoins at ~$1.5B (about 68.7%), which signals Avalanche’s role as a high-utility dollar rail for settlement and everyday onchain movement. The remaining ~31.3% is the “RWA core,” dominated by institutional-grade products: Institutional Alternative Funds at ~$319.8M (about 14.7% of total) and US Treasury Debt at ~$291.4M (about 13.4%), with Private Credit at ~$67.9M (about 3.1%) and non-US government debt at ~$3.8M (about 0.2%) rounding it out. Put simply: most of Avalanche’s real-world value today is still liquid dollars, but a growing share is shifting into regulated, yield-bearing exposure that looks increasingly like traditional finance products running onchain.

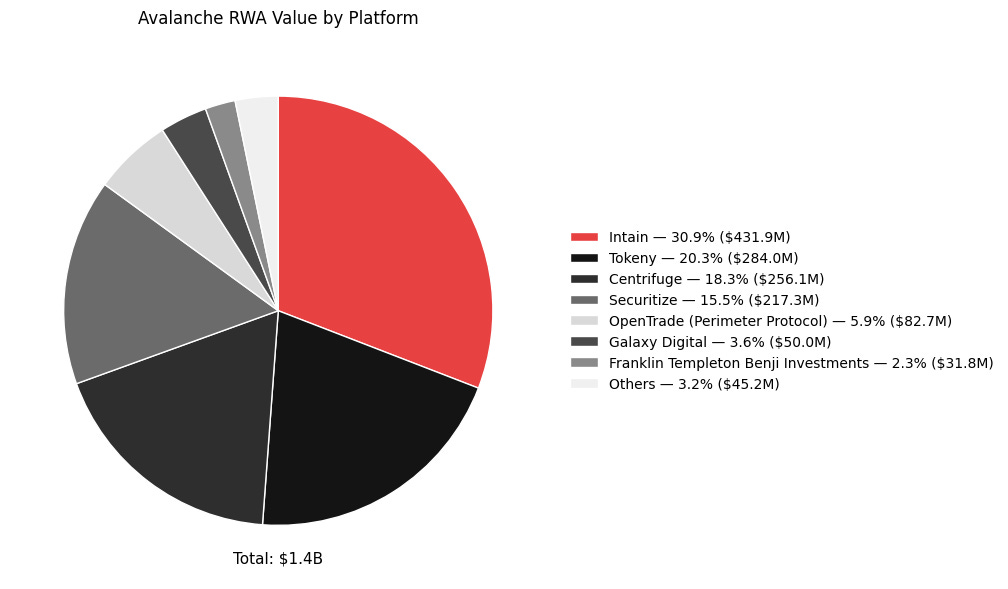

Platform Mix: Who Is Actually Issuing RWAs On Avalanche Right Now

One of the clearest institutional maturity signals on Avalanche is that RWA value is no longer coming from a single issuer or a single product type. It is being carried by a set of platforms that specialize in compliant issuance and distribution, each bringing their own pipeline of assets. In chart, the platform breakdown clusters around a few heavyweight rails: Intain (~$431.9M, ~31.9%), Tokeny (~$284.0M, ~21.0%), Centrifuge (~$256.1M, ~18.9%), and Securitize (~$217.3M, ~16.1%). Together, those top four represent about 88% of total RWA value shown, which tells you where the “real distribution” is happening today: a small number of platforms are already operating at meaningful scale, and Avalanche is one of the places where that issuance lands.

What’s also interesting is how these platforms map to product categories. Intain has private credit in the list, which fits the broader trend of onchain credit moving in large, structured blocks. Centrifuge’s share is driven by institutional-grade credit exposure like the Janus Henderson Anemoy fund. Securitize anchors the “blue-chip tokenization” narrative with products like BlackRock’s BUIDL, plus other fund structures, while Tokeny shows up as a repeat issuer for institutional fund wrappers like Legion Strategies and Digital Macro. There is also smaller but important contributors like OpenTrade (~$82.7M, ~6.1%), which read more like yield and treasury-style vault rails, plus Galaxy Digital (~$50M, ~3.7%) and Franklin Templeton’s BENJI (~$31.8M, ~2.3%) adding recognizable brand weight.

Avalanche’s RWA growth is platform-led now. A handful of issuance rails are concentrating liquidity, while the product mix spans private credit, CLO exposure, and treasury-style funds, which makes the market feel closer to real finance behavior than crypto-native trading behavior

Why Avalanche Shows Up Repeatedly In RWA Conversations

Avalanche keeps showing up for a practical reason: RWA teams care less about narratives and more about operational reliability. When real assets map to legal obligations, the chain becomes part of the settlement process, so the bar is simply higher.

1. RWAs punish unreliable execution

With RWAs, “mostly works” is not good enough. Teams need predictable settlement and clear finality because you’re coordinating real capital, real reporting, and real counterparties. If execution is flaky, you introduce operational risk that institutions will not tolerate.

2. Costs compound fast in production

RWA systems are operational by nature: servicing, reporting, rebalancing, issuance/redemption, compliance checks, and settlement steps. Even when each action is small, the frequency adds up. That’s why teams pay close attention to cost and throughput, because it directly impacts product viability once you move past pilots.

3. Many RWA setups need custom environments

A lot of institutional tokenization work wants tailored controls: identity and permissioning, specific integration patterns, and sometimes dedicated operational parameters. Avalanche’s architecture, including the ability to run specialized Avalanche L1s, matches how these teams often think: separate environments for separate risk and compliance needs, with a path to interoperability when needed.

Avalanche shows up because it aligns with the way RWA teams build: reliable execution, scalable operations, and flexible environments that fit compliance-driven systems.

What I’m Watching In 2026

If 2025 was the year tokenization got more operational, 2026 looks like the year we see which models scale in the real world. Here are the three things I’m watching, and why they matter.

1. Products with clear lifecycle mechanics

The winners in 2026 will be the products that feel boring in the best way: clear issuance, predictable settlement, consistent reporting, and clean redemption paths. In RWAs, most of the risk comes from messy edges, so the projects that define their full lifecycle upfront will earn trust faster.

2. More benchmark-style tokenization

I expect more “benchmark” products, the kinds of exposures that institutions already understand: indices, diversified portfolios, and structured baskets. These are easier to evaluate, easier to compare across venues, and easier to distribute because the narrative is already familiar.

3. Real workflow integrations that make onchain feel invisible

The next wave is less about issuing a token and more about plugging into existing workflows: origination systems, servicing providers, treasury management, and compliance tooling. The most important products in 2026 might be the ones where users barely notice the blockchain, because the integration makes settlement and reporting smoother than the offchain alternative.

From Growth to Structural Maturity

Avalanche’s RWA trajectory from 2024 to 2026 reflects a shift from experimentation to early institutional deployment. Stablecoins remain the liquidity base, while treasury-style funds and private credit now form a meaningful asset layer. The real test now is whether that growth can be sustained. Lifecycle clarity, distribution depth, liquidity consistency, and compliance integration will determine if the recent expansion translates into long-term durability. The question is no longer whether RWAs can scale on Avalanche, but whether they can become routine infrastructure for institutional capital.

References

Dive into the Avalanche ecosystem today! Download the Core Wallet and unlock a world of seamless DeFi, NFTs, and more.

| A guest post by

|

dorito chain la mas madura

Kudos with the recap Team